Summary:

Of all the industries weighing a Cambodian site, apparel and bags has the most complete foundation to land on. In 2025, Cambodia’s garment, footwear and travel-goods (GFT) exports reached about US$15.5 billion (up ~16%), over half of national exports, across roughly 1,800 factories and about 1.1 million workers (mostly women).

For apparel and bags makers, Cambodia’s appeal stacks three things together: a mature industry cluster, the EU EBA single-transformation rule of origin, and competitive labor costs (2026 minimum wage US$210/month, employer social burden ~5.4%). This article covers the industry landscape, tariff preferences, supply-chain strategy, labor costs and setup considerations — and flags how to prepare for the shift in EU preferences after Cambodia’s 2029 LDC graduation.

Apparel & bags, the most complete base to land on in Cambodia

For a labor-intensive manufacturer, “where to build” often comes down to “where can I find enough workers, the right tariff access, and a reliable supply chain.” Apparel and bags is exactly the kind of industry that depends heavily on a large workforce and on export channels — which is precisely why a production base that already has scale and mature trade conditions tends to be more attractive than low wages alone.

In recent years, apparel and bags brands have increasingly made the same request: give me a production base outside China. And every time companies scan their Southeast Asian options, Cambodia almost always appears on the shortlist.

The reason is not hard to see. Apparel and bags is a classic labor-intensive, export-channel-dependent industry, acutely sensitive to three things: finding workers, reaching markets, and sourcing materials. Cambodia keeps coming up precisely because it has built a meaningful base on all three. Just how deep that base runs — and what variables need preparing for in advance — is best understood by first looking at what this industry has actually grown into in Cambodia.

Industry landscape: scale, structure and export markets

Garment, footwear and travel goods (GFT) is the backbone of Cambodian manufacturing: garments and textiles at its core, with footwear and bags as two wings; its main markets are the United States and the European Union.

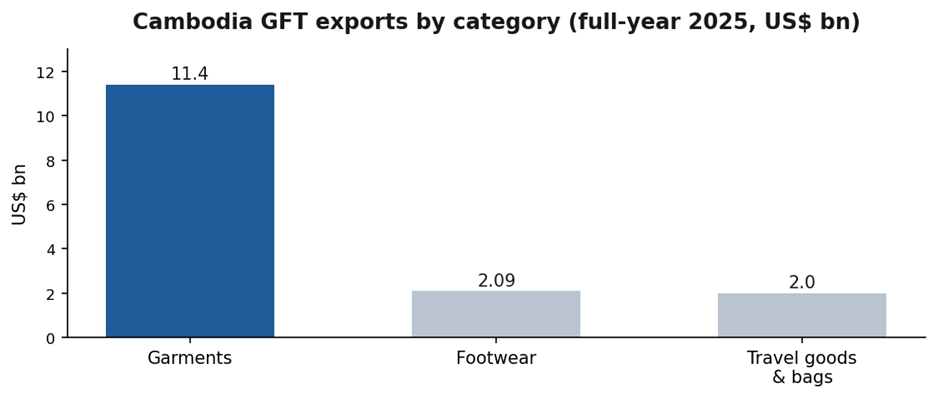

By structure, full-year 2025 garment exports were about US$11.4 billion (up 16.5%), footwear about US$2.09 billion (up 24.5%), and travel goods and bags about US$2.0 billion. Garments are the clear core, footwear is the fastest-growing category in recent years, and travel goods and bags are a steadily expanding wing.

Figure 1: Cambodia GFT exports by category (source: Cambodia GDCE / Ministry of Commerce, full-year 2025).

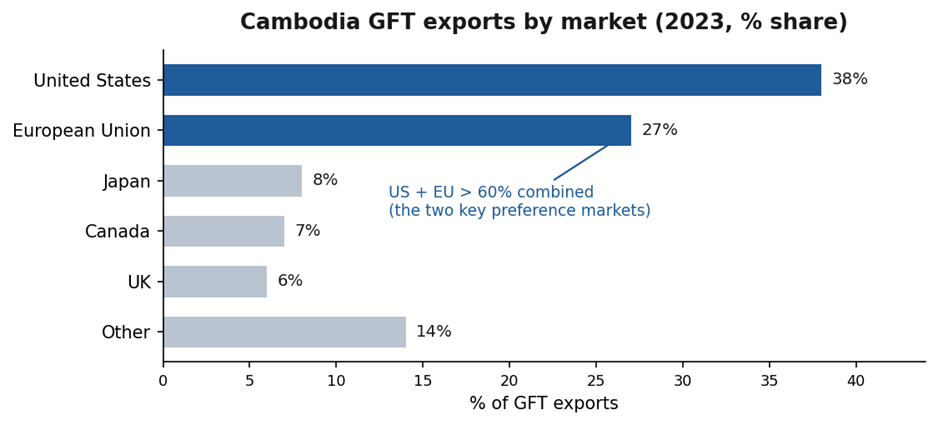

By market, the United States has been Cambodia’s largest GFT export market since 2019, with the EU second, followed by Japan, Canada and the UK. In 2023 the US took about 38% of GFT exports and the EU about 27% — over 60% combined, and the two markets where tariff preferences matter most. Cambodia has continued to diversify, with 2025 exports to the EU growing strongly under EBA (up over 17% in the first ten months).

Figure 2: Cambodia GFT exports by market (2023; the US-first, EU-second structure held in 2024–2025).

Tariff preferences: the three mechanisms apparel & bags benefit from most

Apparel and bags benefit most from three trade mechanisms: the EU EBA’s single-transformation rule of origin, the relative level of the US reciprocal tariff, and cumulation of origin under RCEP and the Cambodia–China FTA.

(i) EU EBA: the value of single-transformation origin

The EU’s “Everything But Arms” (EBA) is Cambodia’s most important market channel for apparel and bags. The key point: as a least-developed country (LDC), Cambodia qualifies for the more lenient “single transformation” rule of origin — a garment made from imported fabric can meet the duty-free criteria.

This contrasts sharply with Vietnam’s EVFTA, which requires “fabric-forward” origin (fabric woven in Vietnam, the EU or Korea). For garment makers who generally use imported fabric, Cambodia’s EU origin threshold is in fact easier to meet. EBA has been partially withdrawn since August 2020, yet about 75% of Cambodian exports still enter duty-free, with garments the bulk of preferential imports.

(ii) US reciprocal tariff: on par with the region, no clear disadvantage

The US is Cambodia’s largest GFT market. The October 2025 US–Cambodia agreement set the reciprocal tariff at 19% — on par with Indonesia and Thailand and slightly below Vietnam’s and Bangladesh’s 20%. It is not a decisive advantage, but neither is it a clear disadvantage. Cambodia’s travel-goods exports also grew rapidly in the past partly under the US GSP travel-goods provision.

(iii) RCEP and the Cambodia–China FTA: complementary cumulation

Cambodia is an RCEP member and has a free trade agreement with China. For the common “Chinese fabric plus Cambodian processing” configuration, the cumulation rules of origin under RCEP and the Cambodia–China FTA help meet origin requirements and obtain preferential rates in Asia-Pacific markets.

| Looking ahead | 2029 LDC graduation: Cambodia will graduate from least-developed-country (LDC) status in December 2029 (UN General Assembly resolution A/79/L.49, confirmed December 2024 — later than the previously estimated 2027, with an exceptional five-year preparatory period). At that point, EU preferences will shift from EBA to the Generalised Scheme of Preferences (GSP/GSP+), with higher tariffs and stricter rules of origin (the lenient single-transformation treatment may no longer apply). For apparel and bags, which rely heavily on imported fabric, this is a variable to plan for in advance — possible responses include building local fabric and accessory supply, leveraging RCEP cumulation, or partly shifting toward other preferential markets. It should be built into medium- to long-term setup planning. |

Supply-chain strategy: the CMT model and “sourcing close by”

Cambodia’s garment industry runs mainly on the CMT (cut–make–trim) model, with over 60% of fabric imported from China; the key to supply-chain strategy is to draw on nearby Chinese and Vietnamese upstream sources to shorten the restocking cycle.

CMT means fabric, machinery and design are largely brought in from abroad, while Cambodia handles the labor-intensive sewing and assembly. By estimate, over 60% of Cambodia’s imported fabric comes from China, and foreign value-added in garment exports is around 45%. This reflects a still-forming upstream (weaving, yarn) — a real constraint to acknowledge when evaluating Cambodia.

Yet this constraint can be eased on two fronts. First, origin design: under EBA’s single-transformation rule, using imported fabric does not affect EU duty-free eligibility; in Asia-Pacific markets, cumulation under RCEP and the Cambodia–China FTA can meet origin requirements. Second, geographic proximity: the Ho Chi Minh City area is a regional sourcing hub for fabric and accessories, and the Cambodia–Vietnam border (such as the Bavet area) is only about one day’s drive from that supply-chain cluster, so companies can source fabric and trim nearby, shortening restocking cycles and reducing in-transit inventory — which is exactly why apparel and bags makers place particular value on parks “close to Ho Chi Minh City” (for cross-border routing, see the article on Cambodia–Vietnam cross-border logistics).

Workforce and cost: the cost structure of a labor-intensive industry

Apparel, footwear and bags depend heavily on a large, stable workforce; labor cost and the supply of skilled workers are often the most central considerations when a company chooses a site.

On this, Cambodia has a clear cost advantage and an established industry base. In 2026, the statutory minimum wage for a regular worker in Cambodia’s garment, textile, footwear, travel-goods and bags industries is US$210 per month; adding the attendance bonus, transport and housing allowances and seniority-based statutory allowances, a worker’s monthly take-home reaches roughly US$227–238 — a relatively clear and predictable labor-cost structure.

On the employer side, Cambodia’s National Social Security Fund (NSSF) statutory employer contribution is about 5.4%, covering mainly occupational risk, health care and pension. By comparison, Vietnam’s combined employer social insurance, health insurance and related mandatory contributions total around 21.5% — so Cambodia’s add-on labor cost is markedly lower.

More importantly, Cambodia does not merely offer low-cost labor: it has built up a workforce on the order of a million in the garment, footwear, travel-goods and bags industries. These workers have long taken part in export manufacturing and are familiar with the rhythm of sewing, assembly, quality control, packing and factory management — forming a depth of skills transfer and line-adaptation capability that other emerging manufacturing sectors have not yet fully established. For apparel and bags companies that need to ramp up quickly, hold delivery dates and employ at scale, this is one of Cambodia’s most attractive industry conditions.

Key considerations for setting up

When evaluating a Cambodian site, apparel and bags companies should keep the following in view to turn the industry’s advantages into stable output.

- Origin design and substantiation: work back from your main export markets (EU / US / Asia-Pacific) to the applicable rules of origin, plan fabric sourcing and cumulation carefully, and keep complete, traceable documentation.

- Prepare for LDC graduation: build the 2029 shift of EU preferences from EBA to GSP/GSP+ into medium- to long-term planning, and assess local fabric supply or market diversification.

- Choose a park with clustering and logistics: because over 60% of fabric and trim is imported from China and Vietnam, proximity to Ho Chi Minh City allows nearby replenishment and shorter restocking and export lead times, lowering early ramp-up costs — so beyond an existing apparel, footwear and bags supplier cluster, favor parks close to the supply chain and ports.

- Compliance as competitiveness: complete working-hour, payroll and social-security records, plus environmental and labor compliance, are now a prerequisite for passing international buyers’ ESG audits (for Cambodia’s environmental impact tiers and setup procedures, see the related articles).

- Total-cost modeling: assess on a “total landed cost” basis — covering wages, social contributions, land, logistics and compliance — rather than comparing nominal wages alone.

MSEZ’s apparel & bags support

Realizing the industry’s advantages ultimately depends on park-level clustering and support; Manhattan Special Economic Zone (MSEZ) has the corresponding conditions in apparel & bags workforce base and logistics location.

MSEZ is located at Bavet on the Cambodia–Vietnam border, covering about 600 hectares, with over 40,000 workers on-site and developed supplier clusters in textiles, footwear, bags and electronics assembly — so a new apparel or bags entrant does not need to build a local network from zero. The zone is about 70–140 km from the HCMC ports (roughly one day’s drive), making it convenient to source fabric and trim nearby from Vietnam and China and to flexibly export through Vietnamese or Cambodian ports.

The zone also has a multilingual (Chinese, English, Khmer) administration and customs-support team that can help with land and factory matters, NSSF registration, working-hour and payroll compliance, cross-border transit declarations and forwarder coordination — lowering the entry threshold for apparel and bags companies. If your company is evaluating a Cambodian site, the MSEZ team is glad to provide an initial assessment based on your product categories, export markets and headcount.

FAQ

Q1. Why would an apparel or bags company choose Cambodia over other Southeast Asian countries?

| Cambodia’s appeal stacks three things together: a mature GFT cluster (about 1,800 factories, ~1.1 million workers), the EU EBA single-transformation rule of origin (imported fabric can still qualify for EU duty-free, an easier threshold than Vietnam’s EVFTA), and competitive labor costs (2026 minimum wage US$210, employer social burden ~5.4%). It fits especially well for garment makers targeting the EU and using imported fabric. |

Q2. Cambodia imports most of its fabric — does that affect origin and delivery times?

| Cambodia’s garment industry runs mainly on CMT, with over 60% of fabric imported from China — that is the reality. But under EBA’s single-transformation rule, using imported fabric does not affect EU duty-free eligibility; in Asia-Pacific markets, cumulation under RCEP and the Cambodia–China FTA applies. On delivery, the border is about one day’s drive from the HCMC supply chain, so materials can be replenished nearby to shorten cycles. |

Q3. How will Cambodia’s 2029 LDC graduation affect apparel and bags?

| Cambodia will graduate from LDC status in December 2029 (confirmed by the UN in 2024, later than the previously estimated 2027). EU preferences will then shift from EBA to GSP/GSP+, with higher tariffs and stricter rules of origin. The impact is greater for apparel and bags that rely on imported fabric. Plan ahead: build local fabric supply, leverage RCEP cumulation, or diversify export markets. It is a variable to build into medium- to long-term setup planning. |

Q4. What kinds of apparel and bags products suit Cambodia?

| Labor-intensive categories with relatively standardized processes fit best — garments (knit and woven), footwear, bags and travel goods. Garments are the existing core, with footwear and bags also growing fast. For high-end technical textiles that are technically demanding and need dense upstream support, fabric supply and technical labor should be assessed together. |

Q5. How much is the labor cost for an apparel or bags factory in Cambodia?

| The 2026 statutory minimum wage is US$210/month for regular workers and US$208 for probationary; adding statutory allowances, take-home reaches about US$227–238. Employers also bear ~5.4% NSSF plus seniority payments. That is markedly lower than Vietnam’s employer social burden of ~22.5%. Assess on a “total landed cost” basis rather than the nominal wage alone. |

References

- Cambodia GDCE / Ministry of Commerce (MoC) | Full-year 2025 GFT exports ~US$15.5bn (+15.7%; MoLVT separately ~US$15.7bn, +15.8%), ~53% of total exports; garments ~US$11.4bn (+16.5%), footwear ~US$2.09bn (+24.5%), travel goods & bags ~US$2.0bn (Cambodia Investment Review, Khmer Times, CamboJA, Jan–Mar 2026)

https://www.khmertimeskh.com/501829076/cambodias-gft-export-surge-despite-tariff-jolt/

- Cambodia Ministry of Labour and Vocational Training (MLVT) | ~1,810 active GFT factories (Oct 2025, up 15.5% from 1,566 at end-2024); ~1.1 million workers (mostly women)

https://www.khmertimeskh.com/501830110/cambodias-garment-and-footwear-exports-surge-to-15-5-billion-in-2025/

- EuroCham / TAFTAC / ILO | Cambodia GFT Sector Brief: 2023 export markets US ~38%, EU ~27%, plus Japan, Canada, UK (2024–2025)

https://www.eurocham-advocacy-compass.com/cambodia-garment-footwear-and-travel-goods-sector-brif-issue-no-3-november-204/

- European Commission / GSP Hub | EU–Cambodia EBA: LDC single-transformation origin, partially withdrawn since Aug 2020, ~75% of exports still duty-free

https://gsphub.eu/country-info/Cambodia

- UN General Assembly resolution A/79/L.49 (adopted 19 Dec 2024) / UN LDC Portal | Cambodia to graduate from LDC status on 19 Dec 2029 (later than the previously estimated 2027, with an exceptional five-year preparatory period); EU preferences then shift from EBA to GSP/GSP+

https://policy.desa.un.org/themes/cdp-news-and-events/news/cambodia-and-senegal-scheduled-to-graduate-from-the-ldc-category-in?language_content_entity=en

- USTR | US–Cambodia reciprocal trade agreement, 19% reciprocal tariff (Oct 2025)

https://www.adb.org/publications/economic-impacts-us-tariff-cambodia

- GMAC / OECD TiVA / ASEAN Briefing | Cambodian garments are mainly CMT; over 60% of fabric (official statements: over 80%) imported from China; foreign value-added in garment exports ~45%

https://asean.org/wp-content/uploads/2024/12/Textiles-Industry-in-CLMV-Economies.pdf

- Cambodia MLVT | Prakas 214/25: 2026 GFT minimum wage US$210 (regular), US$208 (probationary)

https://kh.andersen.com/publications/cambodia-minimum-wage-for-workers-for-2026/