Article Summary:

Moving production capacity overseas can diversify tariff and geopolitical risks, but “moving out” itself also brings a full set of new risks. Industry participants often say, “not going overseas may mean being left behind, but going overseas blindly can also end in failure.” This article groups the risks of setting up factories overseas into six categories: tariffs and policy, compliance and origin, supply chain and cost, labor and operations, land and infrastructure, and governance and reputation. It explains each with real cases and 2026 data.

Two categories are especially difficult. Tariff policy risk is high and hard to predict, as shown by U.S. antidumping and countervailing duty actions on Southeast Asian solar products and the Section 301 investigations into multiple countries including Cambodia. Governance and reputation risks are often underestimated; Cambodia’s Corruption Perceptions Index is only 20-21, and recent scam-compound issues have triggered sanctions by multiple countries.

Most risks, however, can be mitigated through due diligence, origin compliance, market diversification, and choosing the right industrial park. The value of a mature special economic zone lies precisely in sharply lowering the threshold for companies to build infrastructure, connect with government, and handle compliance. The article concludes by explaining how to manage these risks systematically.

Before Setting Up Overseas, Companies Must Ask: Is Moving to Southeast Asia Really Safer?

Many companies move production capacity to Southeast Asia with the original aim of avoiding tariffs and diversifying dependence on a single market or single production location. But when a factory actually lands in a foreign country, companies discover that they must rebuild an entire system of infrastructure, labor, and compliance on unfamiliar ground, and every part of that system contains new risks.

There is a saying in the industry: not going overseas may mean being left behind, but going overseas blindly can also end in failure. Factory relocation is not the finish line; it is the starting point for a series of new decisions. If one category of risk is not clearly understood, the cost advantage on paper may be gradually eaten away by reality. Therefore, rather than asking whether to go overseas, it is better to first lay out what risks will be encountered after going overseas and how to respond. That is exactly what this article sets out to clarify.

Tariff and Policy Risks in Overseas Factory Setup: Relocation Does Not Equal Avoiding Trade Barriers

Tariff and policy risk is the most unpredictable and potentially fatal of the six categories. It comes from the policies of the importing country, is almost impossible for companies to control, and moving to Southeast Asia does not guarantee that it can be avoided.

A vivid case is solar photovoltaics. After Chinese solar companies routed production through Southeast Asia to avoid China-specific tariffs, the United States recently launched antidumping and countervailing duty investigations into crystalline silicon photovoltaic products from Cambodia, Malaysia, Thailand, and Vietnam. Cambodia’s related exports to the U.S. were about USD 2.3 billion in 2023, and the dumping margins determined for some companies exceeded 100%, making further exports to the U.S. almost impossible. This shows that moving out of China can avoid tariffs that specifically target China, such as Section 301, but it may not avoid new measures targeting certain products and certain countries.

The current U.S. tariff environment for Southeast Asia is also changing sharply. The reciprocal tariff originally imposed under IEEPA was invalidated by the Supreme Court in February 2026 and replaced by a temporary Section 122 tariff of around 10%, which is being challenged in court and is under appeal.

In March 2026, the United States also launched Section 301 investigations into 16 economies including Cambodia, and country-specific rates may be implemented after July. Together with Cambodia’s expected graduation from least developed country (LDC) status in 2029 and the corresponding transition of the EU’s EBA duty-free treatment, companies must build tariff and policy assumptions on the premise that they will change. For details on tariffs and origin, see the related articles on hardware factory setup analysis, lighting factory setup analysis, and a full explanation of EBA. This type of risk cannot be eliminated; it can only be diversified and hedged through market diversification and continuous monitoring.

Compliance and Origin Risks in Overseas Factory Setup: Substantial Transformation and Transshipment Review

Moving a factory overseas does not mean the product automatically obtains local origin. Compliance and origin risks are high, but relatively controllable. The key lies in substantial transformation and complete documentation.

The most common misconception is that performing the final process in Southeast Asia and attaching a local label can change origin. But U.S. scrutiny of “China content” is becoming increasingly strict. Minimal assembly or relabeling does not constitute substantial transformation. If tariff avoidance through transshipment is identified, the United States may impose punitive tariffs of up to 40%. Therefore, the model of “Chinese raw materials/components + Southeast Asian processing” must ensure that substantial processes are genuinely completed locally and must retain traceable supply chain and cost documents in order to withstand review.

In addition to origin, compliance also includes labor requirements such as working hours, wages, and social security, environmental requirements such as environmental impact assessment and emissions, and ESG audits by international buyers. In European and U.S. markets, these are now prerequisites for orders, not bonus points. The good news is that this category of risk is highly controllable. As long as origin design and the compliance system are incorporated at the factory planning stage, companies can usually respond steadily. For environmental impact assessment classification and factory setup procedures, see the related articles.

Supply Chain and Cost Risks in Overseas Factory Setup: Why Low Labor Cost Does Not Mean Low Total Cost

Labor unit costs in Southeast Asia are indeed lower than in China, but “low labor cost” does not equal “low total cost.” This is the most common misconception among companies.

There are three reasons. First, most Southeast Asian manufacturing still follows an “imported raw materials/components + local assembly” model. Key materials, equipment, and supporting parts are mostly imported from China, so ocean freight, inland transport, customs declaration, and other landed costs must be included. Second, local worker efficiency and skill levels are usually below those in coastal China, and factory construction and production ramp-up cycles are longer; on a comprehensive basis, costs may not actually be lower. Third, moving old equipment eliminated from domestic production overseas often drags down efficiency because maintenance is inconvenient and skilled technicians are scarce, making the move counterproductive.

Therefore, overseas factory setup should be evaluated based on “total landed cost,” including wages, social security, electricity, raw material import logistics, construction cycle, and efficiency loss, rather than looking only at wages or factory rent. The way to mitigate supply chain risk is to organize raw materials nearby, such as using the Cambodia-Vietnam border’s one-day driving distance to the Ho Chi Minh City supply circle, maintain reasonable safety stock, and carefully plan import logistics. For cross-border logistics, see the article on Cambodia-Vietnam cross-border logistics practices.

Labor, Land, Infrastructure, and Operating Risks in Southeast Asian Factory Setup

Labor, land, and operations are the practical thresholds of landing. Labor involves efficiency and stability, land involves ownership restrictions, and operations involve the reliability of infrastructure such as electricity.

| Risk Item | Main Manifestations | Mitigation Direction |

| Labor risk | Shortage of skilled workers, efficiency and turnover, annual minimum wage adjustments, cultural and labor-management adaptation | Employee training, localized management systems, compliant employment, and stable compensation structures |

| Land and ownership risk | Cambodia’s Constitution prohibits foreigners from owning land; land must be obtained through compliant paths such as long-term lease, a shareholding company, or trust | Prioritize long-term leases in special economic zones, with the park handling land-use compliance |

| Infrastructure and operating risk | Insufficient water, electricity, and roads in some areas; industrial electricity prices are relatively high, and supply stability must be confirmed | Choose mature parks with their own power, water supply, and wastewater treatment, and request the latest industrial electricity rates |

These three categories share one mitigation lever: choosing the right industrial park. Many industrial parks in Southeast Asia build their own power plants, waterworks, and wastewater treatment plants. By clustering together, companies can solve infrastructure problems that would be extremely costly to build alone. Land-use compliance, government coordination, and utilities connection can also often be handled by mature parks. This is the key point discussed below: the industrial park is a decisive variable in reducing landing risk.

Governance, Reputation, and Financial Risks in Overseas Investment: The Hidden Risks Companies Most Often Underestimate

Governance, reputation, and financial risks are significant but often underestimated. Unlike tariffs, they do not directly hit costs, but they slowly erode operations through compliance, banking, and image.改成英文版本

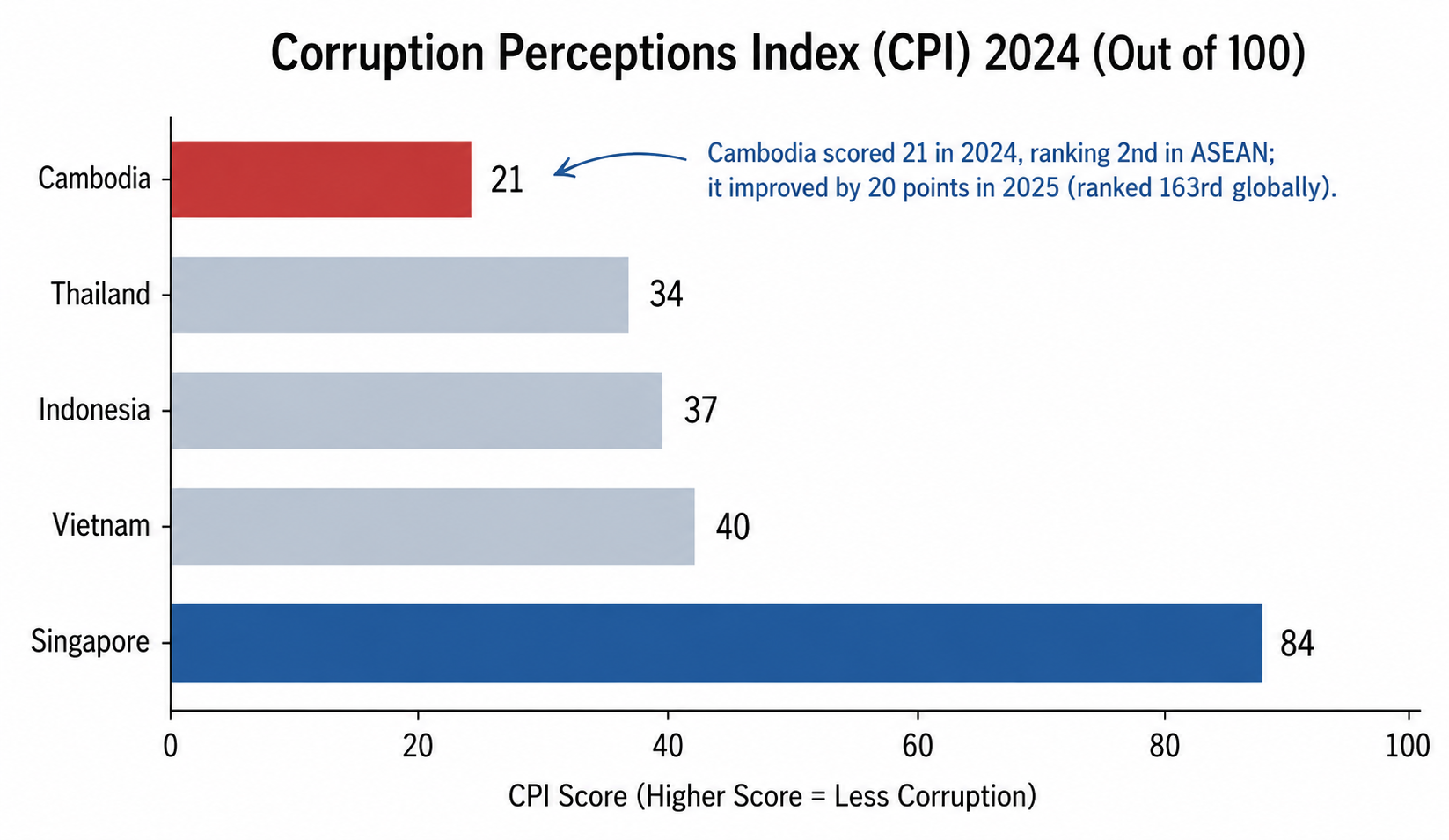

Figure 2: Comparison of Corruption Perceptions Index scores among major ASEAN countries (Source: Transparency International, CPI 2024).

Taking Cambodia as an example, several realities should be viewed objectively. In governance, its Corruption Perceptions Index (CPI) score was only 21 in 2024, ranking 158th out of 180 countries, and fell again to 20 in 2025, second from the bottom in ASEAN. The World Bank Enterprise Survey also lists corruption and administrative inefficiency as major business obstacles. In reputation, Cambodia’s telecom scam compound issues have attracted international attention in recent years. From 2024 to 2025, the U.S. Treasury imposed sanctions on multiple individuals and entities connected to forced-labor scam compounds, as well as Prince Group, and the United Kingdom also took related measures.

However, the scope of impact must be defined accurately. These sanctions target specific individuals and entities, not Cambodia as a country. Cambodia is currently not subject to multilateral sanctions, and lawful manufacturing operating inside regulated special economic zones is a different world from those gray areas.

Still, such issues do affect legitimate companies in three ways: international image and customer perception; stricter cross-border settlement and bank compliance reviews, such as when related payment institutions are placed on U.S. lists; and higher due diligence costs. By contrast, Cambodia also has an open side financially: it allows 100% foreign ownership, is highly dollarized, has relatively loose foreign exchange controls, and allows relatively convenient profit repatriation. The response is to conduct thorough due diligence, choose reputable parks and partners, and establish compliant finance and settlement arrangements.

How Can Companies Systematically Manage Overseas Factory Setup Risks? The Buffering Role of Special Economic Zones

The six categories of risk cannot be eliminated one by one, but they can be managed systematically. External risks such as tariffs and governance require monitoring and diversification, while landing risks such as compliance, supply chain, labor, land, and infrastructure depend on execution and choosing the right industrial park.

The table below summarizes the risks and mitigation directions. It shows that a significant portion of landing risk can be materially reduced through a mature and credible special economic zone. This is the core value of the SEZ model: it turns infrastructure construction, government coordination, land-use compliance, customs clearance, and compliance systems that companies would otherwise face alone into ready-made park-level support.

| Risk Category | Mitigation Direction | What a Special Economic Zone Can Share |

| Tariffs and policy | Market diversification, continuous monitoring, origin layout | Assist with certificates of origin and provide compliance and documentation support |

| Compliance and origin | Substantial transformation, traceable documentation, ESG compliance | Customs assistance and preparation of origin and compliance documents |

| Supply chain and cost | Nearby replenishment, safety stock, total landed cost calculation | Location close to supply circles and existing supplier clusters |

| Labor and operations | Training, localized management, compliant employment | Recruitment coordination and assistance with employment and social security compliance |

| Land and infrastructure | Compliant land access and stable power and water supply | Long-term leases and self-built power, water supply, and wastewater treatment |

| Governance and reputation | Due diligence and selection of reputable parks and partners | Standardized operating environment and credible park endorsement |

MSEZ’s conditions align with these needs. Manhattan Special Economic Zone is located in Bavet on the Cambodia-Vietnam border, covers approximately 600 hectares, and is about 70 to 140 kilometers from the Ho Chi Minh port cluster, making it convenient to organize raw materials nearby and handle cross-border customs clearance. The zone already has supplier clusters in garments, footwear, bags, electronic assembly, lighting, and other industries, and it has built stable power, utilities, and wastewater support.

\At the execution level, the park’s administrative and customs teams use Chinese as their main working language, supplemented by English and Khmer. Having operated since 2005 for more than 20 years, the park can assist companies with long-term land leases, QIP tax incentives, certificates of origin, employment and social security compliance, and cross-border customs clearance. This puts the “park-shareable” items in the table into practice. If your company is evaluating the risks and landing path for overseas factory setup, you are welcome to contact the park team for a preliminary assessment based on your industry, main target markets, and compliance needs.

FAQs on Overseas Factory Setup Risks

Q1: If a factory is moved to Southeast Asia, can it avoid U.S. tariffs?

| Not necessarily. Moving out of China can avoid tariffs that specifically target China, such as Section 301, but it cannot avoid new measures targeting certain products and certain countries. For example, the United States recently launched antidumping and countervailing duty actions on solar products from Cambodia, Vietnam, Thailand, and Malaysia, with some determined rates extremely high. The United States has also launched Section 301 investigations into multiple countries including Cambodia. Tariff policy risk cannot be eliminated; it can only be diversified through market diversification and continuous monitoring. |

Q2: If overseas labor is cheaper, will overall cost necessarily be lower?

| No. This is the most common misconception. Although labor unit costs in Southeast Asia are lower, most manufacturing follows an “imported raw materials + local assembly” model, with materials and equipment mostly imported from China and therefore subject to landed costs. Worker efficiency and skill levels are usually lower than in China, construction and ramp-up cycles are longer, and moving old equipment overseas often drags down efficiency because maintenance is inconvenient. Companies should evaluate based on “total landed cost,” not wages alone. |

Q3: What risk is most easily underestimated in overseas factory setup?

| Governance and reputation risk. It does not directly hit costs like tariffs, but it gradually affects operations through compliance, bank settlement, and international image. Taking Cambodia as an example, its Corruption Perceptions Index score is only 20-21, second from the bottom in ASEAN, and recent scam-compound issues have triggered sanctions by multiple countries against specific individuals and entities. It should be noted that sanctions target specific parties rather than the country, and lawful manufacturing is a different world from gray areas. Companies should still conduct thorough due diligence and choose reputable parks and partners. |

Q4: Can foreign companies buy land and build factories in Cambodia?

| They cannot directly own land. Cambodia’s Constitution prohibits foreigners from owning land. Compliant options include long-term leases of up to 50 years with one renewal, establishment of a locally controlled company, or trusts. Among these, long-term leases in special economic zones are usually the simplest. Companies are advised to prioritize special economic zones and let the park handle land-use compliance to reduce ownership risk. |

Q5: What risks can special economic zones help companies reduce?

| Mainly landing-related risks. Mature parks build their own power, water supply, and wastewater treatment, so companies do not need to shoulder high infrastructure construction costs alone. Long-term land leases, government coordination, customs clearance and compliance documents, labor and social security assistance, and related matters can also often be shared by the park. In other words, external risks such as tariffs and governance require monitoring and diversification, while landing risks such as compliance, supply chain, labor, land, and infrastructure can be significantly reduced by choosing the right industrial park. |

References: Overseas Factory Setup Risks, Tariffs, and Southeast Asia Business Data

- Transparency International | Corruption Perceptions Index (CPI) 2024: Cambodia scored 21, ranked 158th among 180 countries, and was second from the bottom in ASEAN, ahead only of Myanmar; Vietnam 40, Thailand 34, Indonesia 37, Singapore 84. Sources: https://www.ticambodia.org/cpi-2024-press-release-cambodia-en/ ; CPI 2025: Cambodia fell to 20 points (ranked 163rd): https://cambodiainvestmentreview.com/2026/02/10/cambodia-scores-20-100-in-2025-global-corruption-index-ranking-163-of-182-nations-worldwide/

- CamboJA News | Cambodia’s 2024 CPI ranking declined, with comparisons among major ASEAN countries including Vietnam 40, Thailand 34, and Indonesia 37. Source: https://cambojanews.com/cambodias-corruption-ranking-declines-in-2024-government-questions-reports-transparency/

- U.S. Treasury OFAC/FinCEN (published through the U.S. Embassy in Cambodia) | In 2025/10, sanctions were imposed on Prince Group transnational criminal organization and 146 associates; FinCEN used Section 311 of the Patriot Act to cut Huione Group off from the U.S. financial system; the United Kingdom imposed simultaneous sanctions and froze London properties. Source: https://kh.usembassy.gov/press-release-regarding-prince-group-transnational-criminal-organization/ ; overview: https://thediplomat.com/2025/10/us-uk-announce-sweeping-sanctions-in-largest-action-ever-against-southeast-asia-scam-syndicates/

- KnowYourCountry (Cambodia country report) | OFAC sanctions on Ly Yong Phat (2024/9), sanctions in 2025/9 on four Cambodian individuals and six entities connected to forced-labor scam compounds, and Prince Group (2025/10); Cambodia has no multilateral sanctions and sanctions target specific parties; GDP growth was about +5.3% in 2024 and +5.5% in 2025; 100% foreign ownership is allowed and the economy is dollarized. Source: https://www.knowyourcountry.com/country-reports/cambodia/

- CLS | The United States launched antidumping and countervailing duty investigations into crystalline silicon photovoltaic products from Cambodia, Malaysia, Thailand, and Vietnam; Cambodia’s related exports to the U.S. were approximately USD 2.3 billion in 2023, and some dumping margins exceeded 100%. Source: https://www.cls.cn/detail/1697498

- White & Case/Holland & Knight | On 2026/3/11, USTR launched Section 301 investigations into 16 economies including Cambodia, targeting overcapacity; on 2026/2/20, the U.S. Supreme Court held that IEEPA did not authorize tariffs, replacing them with a temporary Section 122 measure (10%, capped at 15%/150 days). Sources: https://www.whitecase.com/insight-alert/ustr-initiates-section-301-investigations-16-us-trade-partners-targeting-industrial ; https://www.hklaw.com/en/insights/publications/2026/03/ustr-launches-awaited-section-301-investigations

- BDO (IEEPA Tariff Refund FAQ) | Section 122 was held ultra vires by the Court of International Trade on 2026/5/7; the Federal Circuit stayed continued collection on 5/12; it is expected to expire around 2026/7/24; CBP imposes a maximum 40% punitive tariff (HTS 9903.02.01) on origin avoidance through transshipment. Source: https://www.bdo.com/insights/tax/ieepa-tariff-refunds-frequently-asked-questions

- Overseas expansion consulting and institutional views | 10000link, “How to Avoid Pitfalls When Building Factories in Southeast Asia” https://info.10000link.com/newsdetail.aspx?doc=2023101690001 ; Guofu Consulting, “Opportunities and Challenges for Chinese Manufacturing Going Overseas” https://project.goalfore.cn/a/5380.html ; JLL https://www.joneslanglasalle.com.cn/zh-cn/insights/chinese-manufacturer-how-to-navigate-southeast-asia ; Colliers https://www.colliers.com.cn/zh-cn/research/bc24-20240416goglobal

- Southern Metropolis Daily | Experts discuss overseas expansion risks: uneven political and business environments, insufficient infrastructure and industrial support, financing difficulty, foreign exchange controls, culture and religion, and related issues. Source: https://m.mp.oeeee.com/oe/BAAFRD0000202501021041003.html